Parametric Regression Models#

Machine Learning Methods#

Module 3: Parametric Regression Models#

Instructor: Farhad Pourkamali#

Overview#

Linear regression: Problem formulation, assumption, loss function, gradient (https://youtu.be/7bzSIX2I2Uk)

Linear regression in Scikit-learn (https://youtu.be/faW0Zo9CTQ8)

Evaluation metrics (https://youtu.be/faW0Zo9CTQ8)

Gradient descent (GD) and variants (https://youtu.be/0EV6UoKM4AM)

Nonlinear extension and regularization (https://youtu.be/OIoe4OQo1ko)

1. Linear regression: Problem formulation, assumption, loss function, gradient#

Case study: univariate linear regression#

Training data: \(\mathcal{D}=\{(x_n,y_n)\}_{n=1}^N\)

Parametric model: \(f(x)=\theta_0+\theta_1 x\)

Objective: Choose \(\theta_0,\theta_1\) such that \(f(x_n)\) is close to \(y_n\)

Mean squared error (MSE):

Solving the optimization problem#

We’ll need the concept of partial derivatives

To compute \(\partial \mathcal{L}/\partial \theta_0\), take the derivative with respect to \(\theta_0\), treating the rest of the arguments as constants

We can show that

Gradient#

Extend the notion of derivatives to handle vector-argument functions

Given \(\mathcal{L}:\mathbb{R}^d\mapsto \mathbb{R}\), where \(d\) is the number of input variables

\[\begin{split}\nabla \mathcal{L}=\begin{bmatrix}\frac{\partial \mathcal{L}}{\partial \theta_0}\\ \vdots\\ \frac{\partial \mathcal{L}}{\partial \theta_{d-1}} \end{bmatrix}\in\mathbb{R}^d\end{split}\]Example from the previous slide (\(d=2\)):

Compact form of gradient#

Let us define

Hence, we get

Compact form of gradient#

The last step is to show that \(\nabla \mathcal{L}\) can be written as

Given this compact form, we can use NumPy to solve the linear matrix equation

# GDP data

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

df = pd.read_csv("https://github.com/ageron/data/raw/main/lifesat/lifesat.csv")

df.head()

| Country | GDP per capita (USD) | Life satisfaction | |

|---|---|---|---|

| 0 | Russia | 26456.387938 | 5.8 |

| 1 | Greece | 27287.083401 | 5.4 |

| 2 | Turkey | 28384.987785 | 5.5 |

| 3 | Latvia | 29932.493910 | 5.9 |

| 4 | Hungary | 31007.768407 | 5.6 |

df.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 27 entries, 0 to 26

Data columns (total 3 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Country 27 non-null object

1 GDP per capita (USD) 27 non-null float64

2 Life satisfaction 27 non-null float64

dtypes: float64(2), object(1)

memory usage: 780.0+ bytes

# Input features and labels (or outcomes) for the regression problem

X = df['GDP per capita (USD)'].to_numpy()

y = df['Life satisfaction'].to_numpy()

print(X.shape, y.shape)

(27,) (27,)

X

array([26456.38793813, 27287.08340093, 28384.98778463, 29932.49391006,

31007.76840654, 32181.15453723, 32238.15725928, 35638.42135118,

36215.44759073, 36547.73895598, 36732.03474403, 38341.30757041,

38992.14838075, 41627.12926943, 42025.61737306, 42404.39373816,

45856.62562648, 47260.80045844, 48210.03311134, 48697.83702825,

50683.32350972, 50922.35802345, 51935.60386182, 52279.72885136,

54209.56383573, 55938.2128086 , 60235.7284917 ])

X.reshape(-1,1)

array([[26456.38793813],

[27287.08340093],

[28384.98778463],

[29932.49391006],

[31007.76840654],

[32181.15453723],

[32238.15725928],

[35638.42135118],

[36215.44759073],

[36547.73895598],

[36732.03474403],

[38341.30757041],

[38992.14838075],

[41627.12926943],

[42025.61737306],

[42404.39373816],

[45856.62562648],

[47260.80045844],

[48210.03311134],

[48697.83702825],

[50683.32350972],

[50922.35802345],

[51935.60386182],

[52279.72885136],

[54209.56383573],

[55938.2128086 ],

[60235.7284917 ]])

np.ones((X.shape[0],1))

array([[1.],

[1.],

[1.],

[1.],

[1.],

[1.],

[1.],

[1.],

[1.],

[1.],

[1.],

[1.],

[1.],

[1.],

[1.],

[1.],

[1.],

[1.],

[1.],

[1.],

[1.],

[1.],

[1.],

[1.],

[1.],

[1.],

[1.]])

# add the column of all 1's

def add_column(X):

'''

add the column of all 1's

'''

return np.concatenate(( np.ones((X.shape[0],1)), X.reshape(-1,1) ), axis=1)

Xcon = add_column(X)

Xcon.shape

(27, 2)

Xcon

array([[1.00000000e+00, 2.64563879e+04],

[1.00000000e+00, 2.72870834e+04],

[1.00000000e+00, 2.83849878e+04],

[1.00000000e+00, 2.99324939e+04],

[1.00000000e+00, 3.10077684e+04],

[1.00000000e+00, 3.21811545e+04],

[1.00000000e+00, 3.22381573e+04],

[1.00000000e+00, 3.56384214e+04],

[1.00000000e+00, 3.62154476e+04],

[1.00000000e+00, 3.65477390e+04],

[1.00000000e+00, 3.67320347e+04],

[1.00000000e+00, 3.83413076e+04],

[1.00000000e+00, 3.89921484e+04],

[1.00000000e+00, 4.16271293e+04],

[1.00000000e+00, 4.20256174e+04],

[1.00000000e+00, 4.24043937e+04],

[1.00000000e+00, 4.58566256e+04],

[1.00000000e+00, 4.72608005e+04],

[1.00000000e+00, 4.82100331e+04],

[1.00000000e+00, 4.86978370e+04],

[1.00000000e+00, 5.06833235e+04],

[1.00000000e+00, 5.09223580e+04],

[1.00000000e+00, 5.19356039e+04],

[1.00000000e+00, 5.22797289e+04],

[1.00000000e+00, 5.42095638e+04],

[1.00000000e+00, 5.59382128e+04],

[1.00000000e+00, 6.02357285e+04]])

np.concatenateExplanationPurpose:

Combines (concatenates) multiple arrays into a single array along a specified axis.

Input:

A tuple or list of arrays to concatenate, all with the same shape except in the concatenation axis.

Axis:

Defines the dimension along which the arrays will be joined.

Default: axis=0 (rows are stacked for 2D arrays).

For axis=1, arrays are concatenated column-wise.

Shape Requirement:

All arrays must have the same shape in dimensions other than the specified axis.

Output:

A new array that is the concatenation of the input arrays along the specified axis.

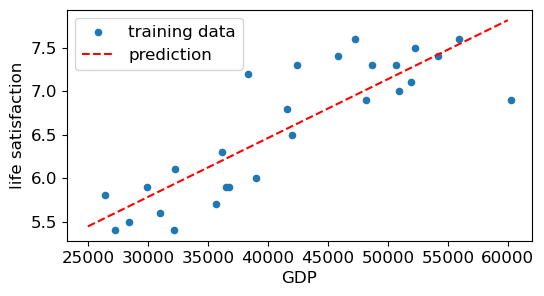

# solve the problem

a = np.matmul(np.transpose(Xcon), Xcon)

b = np.matmul(np.transpose(Xcon), y)

theta = np.linalg.lstsq(a, b, rcond=None)[0] # Cut-off ratio for small singular values

print(theta)

[3.74904943e+00 6.77889970e-05]

# plot the prediction model f

def f(X, theta):

return np.matmul(X, theta)

plt.rcParams.update({'font.size': 12, "figure.figsize": (6,3)})

plt.scatter(X, y, s=20, label='training data')

X_test = np.array([25000, 60000])

y_test = f(add_column(X_test), theta)

plt.plot(X_test, y_test, 'r--', label='prediction')

plt.legend()

plt.xlabel('GDP')

plt.ylabel('life satisfaction')

plt.show()

Linear models for regression#

Given the training data set \(\mathcal{D}=\{(\mathbf{x}_n,y_n)\}_{n=1}^N\) and an input vector \(\mathbf{x}\in\mathbb{R}^D\), the linear regression model takes the form

\(\boldsymbol{\theta}\in\mathbb{R}^D\): weights or regression coefficients, \(\theta_0\): intercept or bias term

Compact representation by defining \(\mathbf{x}=[\color{red}{x_0=1},x_1,\ldots,x_D]\) and \(\boldsymbol{\theta}=[\theta_0,\theta_1,\ldots,\theta_D]\) in \(\mathbb{R}^{D+1}\)

Loss function for linear regression#

MSE loss function for a linear regression model

where we have

Optimization problem for model fitting/training: \(\underset{\boldsymbol{\theta}\in\mathbb{R}^{D+1}}{\operatorname{argmin}} \mathcal{L}(\boldsymbol{\theta})\)

The Normal equation#

To find the value of \(\boldsymbol{\theta}\) that minimizes the MSE, there exists a closed-form solution

a mathematical equation that gives the result directly

The gradient takes the form

Normal equation

2. Linear regression in Scikit-learn#

Import the

LinearRegressionclass fromsklearn.linear_model.Create an instance of the model.

from sklearn.linear_model import LinearRegression

model = LinearRegression()

Use the

.fit()method to train the model on your data.Pass the feature matrix (X) and target vector (y) to the method.

model.fit(X, y)

Use the

.predict()method to predict target values for new data points.

predictions = model.predict(new_X)

Attributes

.coef_: The coefficients (weights) for the linear equation..intercept_: The intercept term (bias) of the linear model.

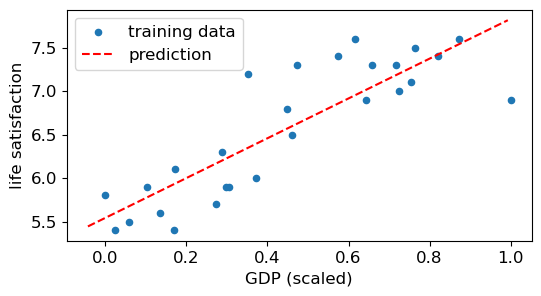

from sklearn.linear_model import LinearRegression

# Revisit the GDP data by preprocessing input features

from sklearn.preprocessing import MinMaxScaler

minmax = MinMaxScaler()

X_minmax = minmax.fit_transform(X.reshape(-1,1))

reg = LinearRegression()

reg.fit(X_minmax, y) # X should be a 2D array

print(reg.intercept_, reg.coef_)

5.542501428448674 [2.28986761]

# Plot the prediction model

plt.rcParams.update({'font.size': 12, "figure.figsize": (6,3)})

plt.scatter(X_minmax, y, s=20, label='training data')

X_test = np.array([25000, 60000]).reshape(-1,1)

X_test_minmax = minmax.transform(X_test)

plt.plot(X_test_minmax, reg.predict(X_test_minmax), 'r--', label='prediction')

plt.legend()

plt.xlabel('GDP (scaled)')

plt.ylabel('life satisfaction')

plt.show()

3. Evaluation metrics#

The quality of a regression model can be assessed using various quantities

Mean squared error

The value you get after calculating MSE is a squared unit of output

If you have outliers in the data set, then it penalizes the outliers most

Possible solution: the output value you get is in the same unit as the required output variable

from sklearn.metrics import mean_squared_error, root_mean_squared_error

y_true = [3, -1, 2, 7]

y_pred = [3, 0, 2, 7]

# If True returns MSE value, if False returns RMSE value.

print('MSE: ', mean_squared_error(y_true, y_pred),

', RMSE: ', root_mean_squared_error(y_true, y_pred))

MSE: 0.25 , RMSE: 0.5

R² score or the coefficient of determination#

Definition

RSS (Residual Sum of Squares) measures the amount of variability that is left unexplained

Best possible score is 1.

An \(R^2\) score of 0 in a regression model means that the model’s predictions are no better than simply predicting the mean of the target variable for all data points.

A negative \(R^2\) is a signal to revisit the model design or data preparation steps.

import numpy as np

from sklearn.linear_model import LinearRegression

from sklearn.metrics import r2_score

# Data where the model performs poorly

X = np.array([[1], [2], [3]])

y = np.array([10, 20, 30]) # Actual target values

y_bad_pred = np.array([40, 50, 60]) # Poor predictions

# Calculate R² manually

ss_res = np.sum((y - y_bad_pred)**2) # Residual sum of squares

ss_tot = np.sum((y - np.mean(y))**2) # Total sum of squares

r2 = 1 - (ss_res / ss_tot)

print("R² score:", r2)

R² score: -12.5

Explained variance score#

Definition

The best possible score is 1.0, lower values are worse.

When the residuals (i.e., \(e_n=y_n-\hat{y}_n\)) have zero mean, the explained variance score and the \(R^2\) score are identical.

4. Gradient descent (GD) and variants#

Optimization problem for model fitting/training: \(\underset{\boldsymbol{\theta}\in\mathbb{R}^{D+1}}{\operatorname{argmin}} \mathcal{L}(\boldsymbol{\theta})\)

Tweak parameters \(\boldsymbol{\theta}\) iteratively to minimize the loss function \(\mathcal{L}(\boldsymbol{\theta})\)

At each iteration \(t\), perform an update to decrease the loss function

where \(\eta_t\) is the step size or learning rate

If the learning rate is too small, then the algorithm will have to go through many iterations to converge

The algorithm may diverge when the learning rate is too high

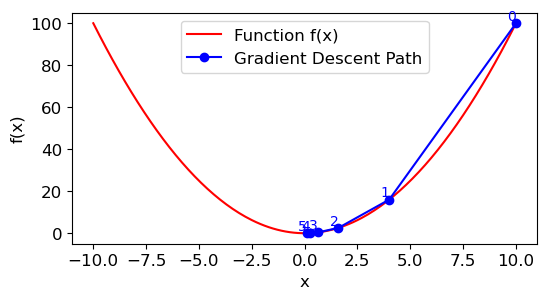

import numpy as np

import matplotlib.pyplot as plt

def f(x): # Objective function

return x ** 2

def f_grad(x): # Gradient (derivative) of the objective function

return 2 * x

def gd(eta, f_grad):

x = 10.0 # initial solution

results = [x]

for i in range(5):

x = x - eta * f_grad(x)

results.append(float(x))

return results

def show_trace(results, f):

# Define the range of the plot based on the solutions

n = max(abs(min(results)), abs(max(results)))

f_line = np.arange(-n, n, 0.1)

# Plot the function

plt.plot(f_line, [f(x) for x in f_line], 'r-', label='Function f(x)')

# Plot the solution path

plt.plot(results, [f(x) for x in results], 'bo-', label='Gradient Descent Path')

# Annotate each solution point with the iteration number

for i, x in enumerate(results):

plt.text(x, f(x), f'{i}', color='blue', fontsize=10,

ha='right', va='bottom')

# Add labels and legend for better clarity

plt.xlabel('x')

plt.ylabel('f(x)')

plt.legend()

# Show the plot

plt.show()

show_trace(gd(0.3, f_grad), f)

Batch GD for linear regression#

Recall the gradient vector of the loss function

GD step with fixed learning rate

This formula involves calculations over the full training set \(\mathbf{X}\) –> batch or full GD

An epoch means one complete pass of the training data set

# GDP data

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

df = pd.read_csv("https://github.com/ageron/data/raw/main/lifesat/lifesat.csv")

X = df['GDP per capita (USD)'].to_numpy()

y = df['Life satisfaction'].to_numpy()

def add_column(X):

'''

add the column of all 1's

'''

return np.concatenate(( np.ones((X.shape[0],1)), X.reshape(-1,1)), axis=1)

from sklearn.preprocessing import MinMaxScaler

minmax = MinMaxScaler()

X_minmax = minmax.fit_transform(X.reshape(-1,1))

Xcon = add_column(X_minmax)

print(Xcon[:5])

[[1. 0. ]

[1. 0.02459182]

[1. 0.05709406]

[1. 0.10290627]

[1. 0.13473858]]

# Implementation of Batch GD

eta = 0.01 # learning rate

n_epochs = 1000

N = len(Xcon) # number of instances

np.random.seed(3)

theta = np.random.randn(2, 1) # randomly initialized model parameters

for epoch in range(n_epochs):

gradients = 2 / N * Xcon.T @ (Xcon @ theta - y.reshape(-1,1))

theta = theta - eta * gradients

print(theta)

[[5.54877943]

[2.27673633]]

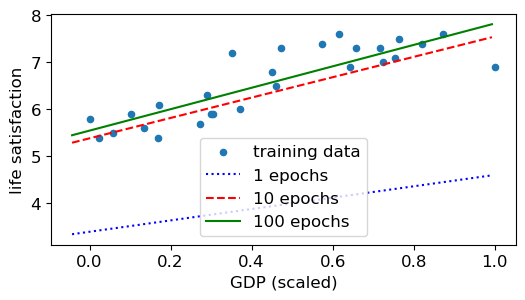

# Impact of eta (step size)

np.random.seed(3)

theta = np.random.randn(2, 1) # randomly initialized model parameters

X_test = np.array([25000, 60000]).reshape(-1,1)

X_test_minmax = add_column(minmax.transform(X_test))

plt.scatter(X_minmax, y, s=20, label='training data')

eta= .1 # 0.001, 0.01, 0.1

for epoch in range(n_epochs):

gradients = 2 / N * Xcon.T @ (Xcon @ theta - y.reshape(-1,1))

theta = theta - eta * gradients

if epoch == 1:

plt.plot(X_test_minmax[:,1], X_test_minmax@theta , 'b:', label='1 epochs')

elif epoch == 10:

plt.plot(X_test_minmax[:,1], X_test_minmax@theta , 'r--', label='10 epochs')

elif epoch == 100:

plt.plot(X_test_minmax[:,1], X_test_minmax@theta , 'g-', label='100 epochs')

plt.legend()

plt.xlabel('GDP (scaled)')

plt.ylabel('life satisfaction')

plt.show()

Stochastic gradient descent (SGD) for linear regression#

The main problem with GD is that it uses the whole training set at every step

Consider a minibatch of size \(B=1\) and a selected sample \(\mathbf{x}_n^T\) from \(\mathbf{X}\) (row vector)

Given that \(N\) is the sample size and \(B\) is the batch size, in one epoch we update our model \(N/B\) times

n_epochs = 5

t0, t1 = 5, 50 # learning schedule hyperparameters

def learning_schedule(t):

return t0 / (t + t1)

np.random.seed(42)

theta = np.random.randn(2, 1) # random initialization

# Loop over the number of epochs (complete passes over the data)

for epoch in range(n_epochs):

# Loop over individual data points

for iteration in range(N): #(N/B, B=1)

# Select a random index for the current data point

random_index = np.random.randint(N)

# Extract xi and yi

xi = np.transpose(Xcon[random_index : random_index + 1])

yi = y[random_index : random_index + 1]

# Compute the gradient of the loss function

gradients = 2 * xi @ (xi.T @ theta - yi) # for SGD, do not divide by N

# The learning schedule decreases the learning rate over time

eta = learning_schedule(epoch * N + iteration)

# Update the parameter vector (theta)

theta = theta - eta * gradients

print(theta)

[[5.56898107]

[2.27782555]]

Sklearn implementation of SGD for linear regression

https://scikit-learn.org/stable/modules/generated/sklearn.linear_model.SGDRegressor.html

Parameters

max_iter: epochs

learning_rate: constant or variable

n_iter_no_change: number of iterations with no improvement to wait before stopping fitting

# GDP data

from sklearn.pipeline import Pipeline

from sklearn.linear_model import SGDRegressor

X = df['GDP per capita (USD)'].to_numpy().reshape(-1,1)

y = df['Life satisfaction'].to_numpy()

pipe = Pipeline([('preprocess', MinMaxScaler()),

('reg', SGDRegressor(random_state=42))])

pipe.fit(X, y)

print(pipe['reg'].intercept_, pipe['reg'].coef_)

[5.35324059] [2.47088247]

5. Nonlinear extension and regularization#

The linear model may not be a good fit for many problems

We can improve the fit by using a polynomial regression model of degree \(d\)

where \(\phi(x)=[1,x,x^2,\ldots,x^d]\)

This is a simple example of feature preprocessing/engineering

Benefit: linear function of parameters but nonlinear wrt input features

We can use sklearn.preprocessing.PolynomialFeatures to generate polynomial features

Use pipeline in sklearn to assemble several steps (preprocessing + estimator)

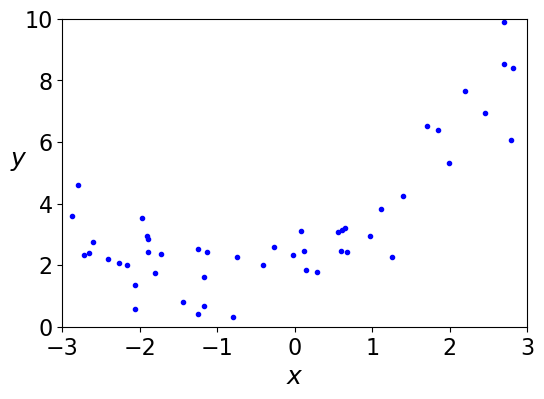

In the following, we generate a synthetic model of the form:

where the noise represents random variations added to simulate real-world data.

# Generate simulated data

import numpy as np

import matplotlib.pyplot as plt

np.random.seed(42)

plt.rcParams.update({'font.size': 16, "figure.figsize": (6,4)})

N = 50

X = 6 * np.random.rand(N, 1) - 3

y = 0.5 * X**2 + X + 2 + np.random.randn(N, 1)

plt.plot(X, y, "b.")

plt.xlabel("$x$", fontsize=18)

plt.ylabel("$y$", rotation=0, fontsize=18)

plt.axis([-3, 3, 0, 10])

plt.show()

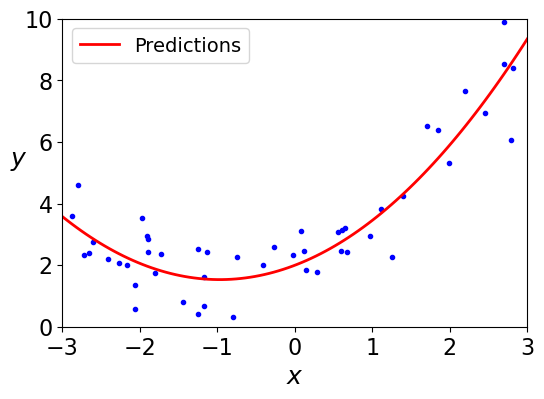

# train polynomial model

from sklearn.preprocessing import PolynomialFeatures

from sklearn.pipeline import Pipeline

from sklearn.linear_model import LinearRegression

pipe = Pipeline([

('poly', PolynomialFeatures(degree=2, include_bias=False)),

('regr', LinearRegression())])

pipe.fit(X, y) # training

X_new = np.linspace(-3, 3, 100).reshape(100, 1)

y_new = pipe.predict(X_new) # prediction

plt.plot(X, y, "b.")

plt.plot(X_new, y_new, "r-", linewidth=2, label="Predictions")

plt.xlabel("$x$", fontsize=18)

plt.ylabel("$y$", rotation=0, fontsize=18)

plt.legend(loc="upper left", fontsize=14)

plt.axis([-3, 3, 0, 10])

plt.show()

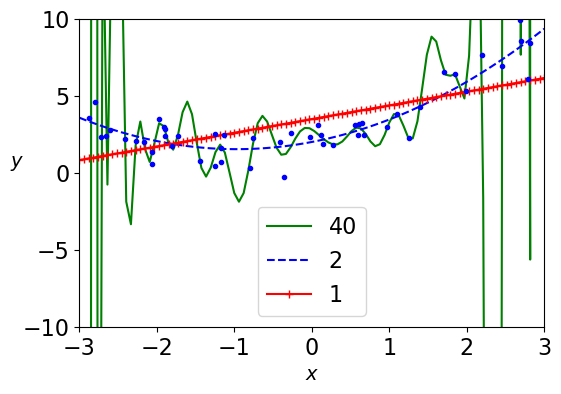

# Compare varying complexity levels

from sklearn.preprocessing import StandardScaler

for style, degree in (("g-", 40), ("b--", 2), ("r-+", 1)):

polybig_features = PolynomialFeatures(degree=degree, include_bias=False)

std_scaler = StandardScaler()

lin_reg = LinearRegression()

polynomial_regression = Pipeline([("poly_features", polybig_features),

("std_scaler", std_scaler),

("lin_reg", lin_reg)])

polynomial_regression.fit(X, y)

y_newbig = polynomial_regression.predict(X_new)

plt.plot(X_new, y_newbig, style, label=str(degree))

plt.plot(X, y, "b.", linewidth=3)

plt.legend()

plt.xlabel("$x$", fontsize=14)

plt.ylabel("$y$", rotation=0, fontsize=14)

plt.axis([-3, 3, -10, 10])

plt.show()

The bias-variance tradeoff#

A model’s generalization (or test) error can be decomposed into three components:

Bias: Error introduced by approximating a real-world problem, which may be complex, by a simplified model.

High bias models make strong assumptions about the data, potentially leading to underfitting, where the model fails to capture underlying patterns.

Variance: Error introduced by the model’s sensitivity to small fluctuations in the training set.

High variance models are overly sensitive to training data variations, leading to overfitting, where the model captures noise rather than the intended outputs.

Irreducible Error: Error inherent in the data itself, due to noise or other unpredictable factors, which cannot be reduced by any model.

Model flexibility and error relationship

As a model’s flexibility (complexity) increases, its training error typically decreases because it can fit the training data more closely.

However, the test error often follows a U-shaped curve:

With low flexibility, both training and test errors are high due to underfitting.

With moderate flexibility, test error decreases as the model captures the underlying data patterns.

Beyond a certain point, increasing flexibility leads to overfitting, causing test error to rise even as training error continues to decline.

This balance between bias and variance is known as the bias-variance tradeoff. Achieving optimal model performance involves finding the right level of complexity that minimizes test error by appropriately balancing bias and variance.

Regularization#

Regularization adds a penalty term to the model’s loss function to discourage excessive complexity.

Common regularization techniques:

L1 Regularization (Lasso): Adds the sum of the absolute values of coefficients as a penalty.

L2 Regularization (Ridge): Adds the sum of the squares of coefficients as a penalty.

Elastic Net: Combines L1 and L2 penalties.

By discouraging large weights, it prevents the model from overfitting small variations or noise in the training data.

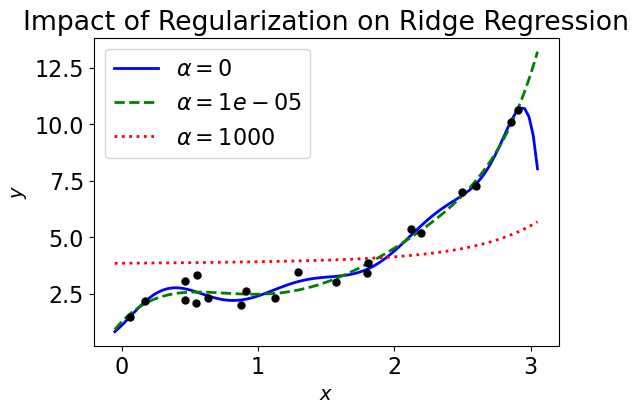

Mathematical representation

* $\lambda\geq 0$ is the regularization parameter (i.e., hyperparameter) and $C(\boldsymbol{\theta})$ is some form of model complexity.

* We can quantify complexity using the L2 regularization formula, i.e., the sum of the squares of all weights

# Synthetic/Simulated Data (Ridge Regression or L2)

from sklearn.linear_model import Ridge

import numpy as np

import matplotlib.pyplot as plt

from sklearn.pipeline import Pipeline

from sklearn.preprocessing import PolynomialFeatures, StandardScaler

# Seed for reproducibility

np.random.seed(42)

# Generate synthetic data with a cubic relationship

N = 20

X = 3 * np.random.rand(N, 1)

y = 2 + 0.5 * X**3 - 0.8 * X**2 + X + np.random.randn(N, 1) / 2 # Cubic function with noise

X_new = np.linspace(0-0.05, 3+0.05, 100).reshape(100, 1)

# Regularization strengths to explore

alphas = (0, 10**-5, 1000)

# Iterate through different alpha values and plot the results

for alpha, style in zip(alphas, ("b-", "g--", "r:")): # zip aggregates alphas and styles

model = Pipeline([

("poly_features", PolynomialFeatures(degree=10, include_bias=False)), # 10th degree polynomial

("std_scaler", StandardScaler()), # Standardize features

("regul_reg", Ridge(alpha=alpha)), # Ridge regression with specified alpha

])

model.fit(X, y)

plt.plot(X_new, model.predict(X_new), style, linewidth=2, label=r"$\alpha = {}$".format(alpha))

# Plot the original data

plt.plot(X, y, "k.", markersize=10) # Original data points

plt.legend()

plt.xlabel("$x$", fontsize=14)

plt.ylabel("$y$", fontsize=14)

plt.title("Impact of Regularization on Ridge Regression")

plt.show()

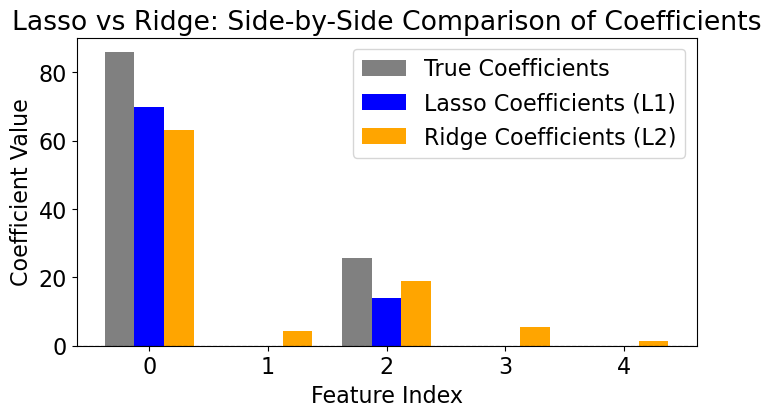

Synthetic data generation for comparing L1 (Lasso) vs L2 (Ridge):

The

make_regressionfunction is used to create a data set for regression tasks:n_samples=50: 50 data points are generated.n_features=5: The data has 5 features.n_informative=2: Out of the 5 features, only 2 are truly informative (affect the target variable).noise=1: Adds Gaussian noise to the target variable to make the problem more realistic.effective_rank=2: Introduces correlations between features by generating a low-rank design matrix.coef=True: Returns the coefficients of the underlying true model.

import numpy as np

from sklearn.linear_model import Lasso, Ridge

from sklearn.datasets import make_regression

import matplotlib.pyplot as plt

# Generate synthetic data with redundant features

np.random.seed(5)

X, y, coefficients = make_regression(

n_samples=50, # Number of samples

n_features=5, # Total features

n_informative=2, # Only 2 features are informative

noise=1, # Add some noise

effective_rank =2,

coef=True, # Return the coefficients for the true model

)

print(coefficients)

[85.84989327 0. 25.73873511 0. 0. ]

# Apply Lasso Regression

lasso = Lasso(alpha=0.1) # L1 regularization strength

lasso.fit(X, y)

# Apply Ridge Regression

ridge = Ridge(alpha=0.1) # L2 regularization strength

ridge.fit(X, y)

# Plotting side-by-side comparison

width = 0.25 # Width of the bars

x_indices = np.arange(len(coefficients)) # Indices for features

plt.figure(figsize=(8, 4))

# Plot True coefficients

plt.bar(x_indices - width, coefficients, width=width, label="True Coefficients", color='gray')

# Plot Lasso coefficients

plt.bar(x_indices, lasso.coef_, width=width, label="Lasso Coefficients (L1)", color='blue')

# Plot Ridge coefficients

plt.bar(x_indices + width, ridge.coef_, width=width, label="Ridge Coefficients (L2)", color='orange')

# Add labels and formatting

plt.axhline(0, color='black', linestyle='--', linewidth=0.8)

plt.xlabel("Feature Index")

plt.ylabel("Coefficient Value")

plt.title("Lasso vs Ridge: Side-by-Side Comparison of Coefficients")

plt.xticks(x_indices)

plt.legend()

plt.show()

When features are highly correlated (as happens with

effective_rank=2), Ridge struggles to distinguish between them, which can result in suboptimal generalization and interpretation.Lasso regression performs feature selection by setting some coefficients to zero. It eliminates redundant or less important features entirely.

Recommended Reading#

Chapters 3 and 5 of An Introduction to Statistical Learning With Applications in Python: https://www.statlearning.com/

Chapter 4 of Hands-on Machine Learning with Scikit-Learn, Keras and TensorFlow: ageron/handson-ml3

Chapter 11 of Probabilistic Machine Learning: An Introduction: https://probml.github.io/pml-book/book1.html